Ravindra Ojha's Courses

Explore professional courses and services designed to elevate your skills and knowledge today.

Discover Ravindra Ojha's Expertise

With over a decade of experience in tax consultancy and financial education, I have dedicated my career to empowering individuals with the knowledge and skills necessary to navigate the complexities of finance and the stock market.

Professional Background :- Since 2013, I have been committed to educating aspiring Chartered Accountants, providing them with the insights and understanding required to excel in their examinations and future careers. In 2017, I expanded my focus to include stock market training, recognizing the growing need for comprehensive financial literacy. This journey has led me to conduct numerous webinars and seminars, through which I have had the privilege of training thousands of students in finance and stock market principles.

Educational Initiatives :- My passion for financial education has been recognized by various institutions, leading to invitations from numerous colleges and Delhi government schools to train students in stock market fundamentals. These opportunities have allowed me to reach a diverse audience, fostering financial awareness among young minds.

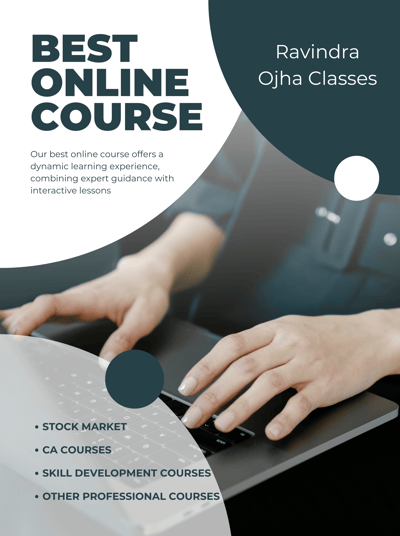

Online Presence and Courses :- To make financial education more accessible, I have developed a range of online courses and resources. My official website, ravindraojha.com, offers professional courses and services designed to elevate skills and knowledge in tax consultancy and the stock market. Additionally, I have created specialized courses on platforms like Udemy, including a comprehensive 5-in-1 Stock Trading & Investment course bundle, aimed at providing in-depth understanding to beginners and advanced traders alike.

Student Success and Feedback :- The most rewarding aspect of my career is witnessing my students' success. Many have expressed appreciation for my teaching methodology, highlighting the practical approach and live market demonstrations that have enabled them to achieve financial freedom through successful trading.

Connect with Me :- I am active on various social media platforms and encourage you to connect with me for updates on courses, live sessions, and financial insights:

Instagram: @theRavindraOjha

Twitter: @theRavindraOjha

LinkedIn: @theRavindraOjha

YouTube: Live Trading with Ravindra Ojha

YouTube: WisdomCA

Through these platforms, I aim to continue my mission of providing accessible and practical financial education to all.

Testimonials

Discover what our clients think about our service

Get in touch

Have a question? Feel free to get in touch with us by filling the form given below.

Office No. 4, 5th Floor, Plot No C, 1, Noida Greater Noida Expy. Sector 153, Noida, U.P. - 201310

visit us

About

© 2025. All rights reserved.

contact us

+91-7428118333

company

Email - info@ravindraojha.com